Prop firm drawdown rules explained: daily, overall, trailing, static

Drawdown rules are the single most common reason traders lose prop firm accounts, and misunderstanding them costs more challenge fees than bad trades do. Every prop firm applies at least two drawdown limits: a daily limit and an overall limit. Breach either one and the account is terminated immediately, regardless of total profit or how close the trader is to a payout. A lot of applicants read the headline numbers (4% daily, 8% overall) and assume they understand the rules, but the calculation method behind those numbers matters just as much as the numbers themselves. This article explains how each type of drawdown works, how the firm calculates it and where traders lose accounts without expecting to.

What drawdown means in prop trading

In prop trading, drawdown is the decline from a reference point — either a peak equity or a fixed starting balance — to the current account value. It is always expressed as a percentage of the starting account balance, not of the peak. So on a $100k account, a 4% daily drawdown limit means the account equity cannot fall more than $4k below the reference point in a single trading day, and an 8% overall limit means the account cannot fall more than $8k below its overall reference point at any moment. Exceeding either limit closes the account, usually automatically.

The key word is reference point, because firms calculate that differently, and this is where static and trailing drawdown diverge.

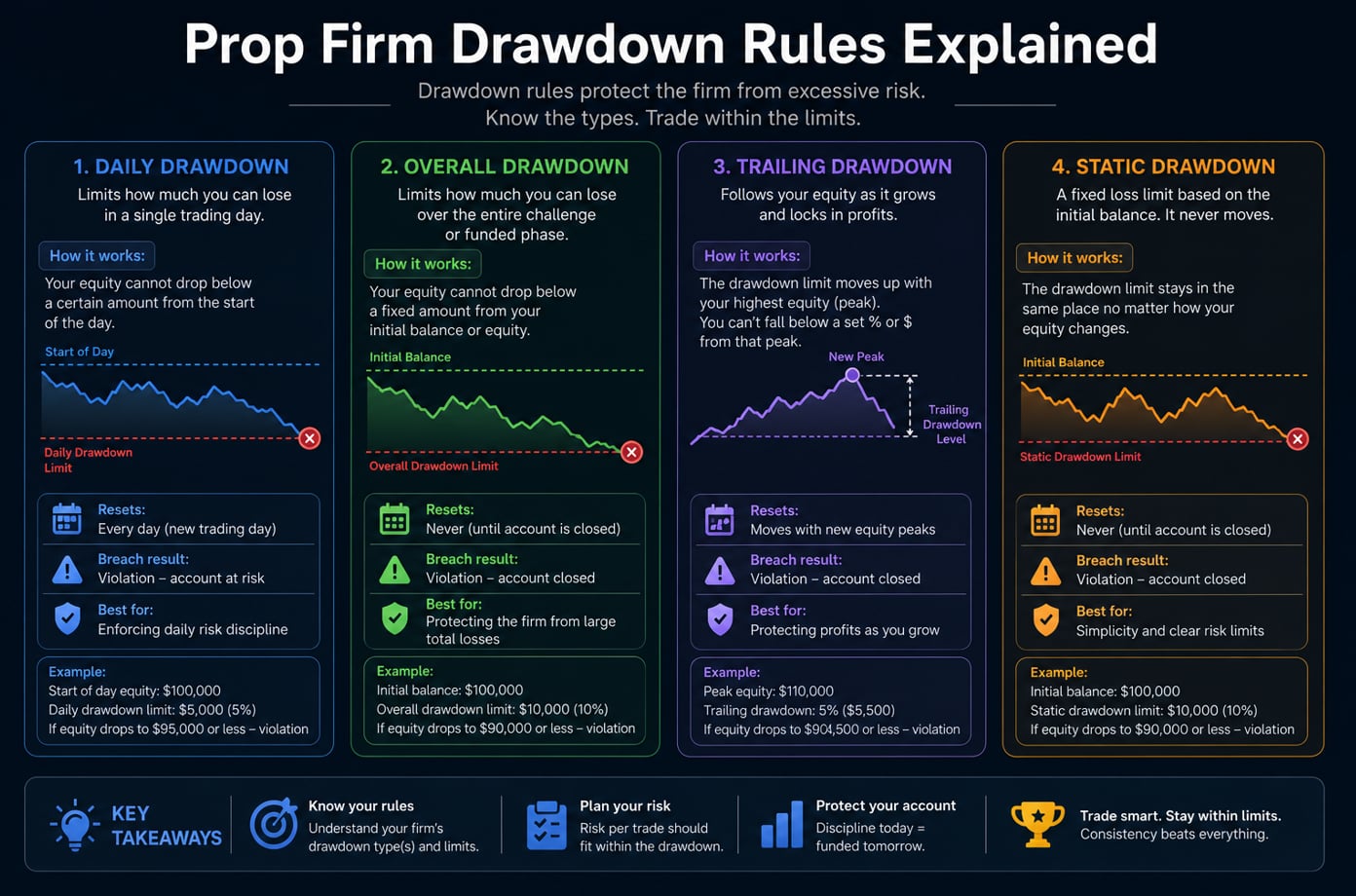

Daily drawdown

Daily drawdown limits how much the account can lose within a single trading day. The typical limit is 4-5% of the starting account balance, and it resets at a fixed server time, most commonly 5 PM EST or midnight GMT, depending on the firm and broker. The reset happens regardless of what the account did that day, so a trader who lost 3.9% in the morning starts the next day with a fresh 4% limit.

How the daily reference point is calculated varies between firms. The two most common methods are:

Balance-based daily drawdown — the reference point is the account balance at the start of the trading day (after the reset). This method ignores unrealized profit: if a trader opens a position that floats 2% up during the day and then reverses 4% from the float high, the firm calculates the drawdown from the starting balance, not from the intraday peak. This is the more forgiving calculation method.

Equity-based daily drawdown — the reference point is the highest equity reached during the trading day, including floating positions. Under this method, if a trader's account reaches $104k intraday on an open trade and then that trade reverses to $100k, the daily drawdown is calculated as 4% from the $104k peak, not from the starting $100k. The account is already at the limit, even though the balance is unchanged. This method is significantly stricter and catches a lot of traders off guard, particularly those who hold positions through volatile sessions without a tight stop-loss in place.

Before starting any challenge, it is important to confirm which daily drawdown calculation the firm uses, as this one parameter can completely change how much real risk the trader is taking per session.

Overall drawdown

Overall drawdown limits how far the account can fall from a reference point across its entire lifetime. The typical limit is 8-12% on standard challenges. Once the account touches that level, the evaluation or funded account is over. Unlike daily drawdown, overall drawdown does not reset — it is a permanent floor that moves only under trailing drawdown rules (explained below).

Static and trailing are the two types of overall drawdown, and choosing a firm without knowing which one it uses is one of the most common mistakes in challenge selection.

Static drawdown

Static drawdown sets the overall floor once, at the start of the account, and it never changes. On a $100k account with 10% static drawdown, the floor is always $90k, from day one until the account is closed or funded. As the trader generates profit, the gap between current balance and the floor grows, creating an increasing buffer. At $110k balance, the effective risk buffer is $20k — double the original 10%.

Static drawdown is the more forgiving structure and is generally better suited to swing traders, news traders and anyone whose strategy involves holding positions through temporary adverse moves. It gives the trader room to recover from a losing streak without the floor chasing equity upward. A lot of beginner-friendly prop firms advertise static drawdown as a key feature, and for early-stage traders it genuinely is.

Trailing drawdown

Trailing drawdown moves the overall floor upward with the account's equity or balance as it grows, up to a certain ceiling. The exact mechanics depend on the firm: some trail on balance (closed trades only), others trail on equity (including floating positions). Trailing typically locks once the floor reaches the initial starting balance, meaning the firm's capital is fully protected from that point onward.

The standard example: $100k account, 10% trailing drawdown, trail on equity. The starting floor is $90k. The trader opens a position and the account equity reaches $104k. The floor moves up to $93.6k (i.e. $104k minus 10%). The trade reverses and closes at $101k. The floor is now at $93.6k and stays there. The trader then has a losing day and drops to $93.5k — the account is terminated, even though the balance is still above the starting level.

The important and often misunderstood detail with trailing drawdown is that the floor can move against the trader on unrealized profit, not just on closed profit. A floating profit of $5k that later reverses to zero still moved the floor up during the time it was open. Traders who run strategies with large open profits and wide stops are particularly exposed to this effect. Another benefit of understanding trailing mechanics is that it clarifies the optimal behavior early in the challenge: many experienced traders deliberately keep initial positions small until the trailing drawdown locks at the starting balance, effectively eliminating the tail risk of losing firm capital.

Daily vs overall: which triggers first

Daily and overall drawdown run in parallel, not in sequence. A trader can blow the daily limit on a large intraday loss without touching the overall limit, or erode the overall limit slowly across many small losing days without ever triggering the daily one. In practice, most sudden account terminations happen on daily drawdown, while most slow account deaths happen on overall drawdown. It is important to monitor both in real time, and most trading platforms connected to prop firm accounts display remaining drawdown headroom either as a dashboard widget or a fixed line on the equity chart.

How drawdown resets work in practice

Daily drawdown resets at the firm's server reset time, not at midnight in the trader's local timezone. This creates an asymmetry for traders in non-US timezones: a trader in Europe trading with a 5 PM EST reset has his daily limit running from 11 PM to 11 PM local time, which means an overnight position opened at 10 PM can accumulate loss in two separate daily windows. Missing the reset time is a low-probability but real cause of unexpected daily drawdown breaches, especially for traders who hold positions overnight into the US session open.

Drawdown and floating positions

Whether open (unrealized) positions count toward drawdown calculations is one of the most important questions to answer before joining any firm. On most platforms equity includes floating P&L, so a large open loss pushes equity down and can trigger a drawdown breach even with a positive closed balance. Some firms explicitly calculate drawdown on balance only, which means open positions are irrelevant until they are closed. This distinction matters most for swing traders who hold multi-day positions with wide stops and for traders who size up on high-conviction setups.

Which drawdown type suits which trading style

Static overall drawdown with balance-based daily drawdown is the most forgiving combination and suits swing traders, position traders and beginners who are still learning to manage intraday volatility. It gives the most room to recover from drawdowns and reduces the risk of mechanical termination from unrealized fluctuations.

Trailing drawdown with equity-based daily drawdown is the strictest combination. It suits disciplined intraday traders with tight stop-losses, high win rates and no need to hold large floating positions. Under this structure, consistency matters more than any single trade.

Regardless of the drawdown type, the fundamental discipline is the same: size positions so that a full stop-loss hit stays well inside the daily limit, not exactly at it. A lot of traders calibrate their size to the maximum allowed drawdown and leave themselves no room for multiple losses in the same session. Running at 50-60% of the daily limit per trade creates enough buffer to absorb a second consecutive loss without breaching, which is the difference between a recoverable bad day and a terminated account.

About Marina G.

Professional content writer specializing in prop trading and financial markets.

Related Articles

More insights from our prop trading experts